When financing a car through a dealership in Uganda, you’ll need to prepare certain documents to ensure a smooth process. Here’s what you need to know:

- Proforma Invoice: A detailed preliminary bill from the dealer outlining costs.

- Financing Application Form: Official loan application confirming down payment ability (typically 40% of the car’s value).

- National ID or Financial Card: For identity verification and credit history checks.

- Bank Statements (6–12 Months): Proof of financial stability.

- Proof of Income: Pay stubs, tax returns, or other income documentation.

- Vehicle-Specific Documents (For Used Cars): Includes the logbook, market valuation, and import documents if applicable.

For businesses, additional documents like a certificate of incorporation, tax registration, and audited financial statements are required. Preparing these in advance helps avoid delays.

Finally! Affordable Cars and Good Payment Methods in Uganda

sbb-itb-7bab64a

Required Documents for All Applicants

If you’re looking to secure dealership financing in Uganda, having the right documents is key. Whether you’re applying as an individual or on behalf of a company, these documents help lenders verify details and process your application efficiently. Here’s what you’ll need to get started.

Proforma Invoice from the Dealer

A proforma invoice is essentially a preliminary bill of sale provided by the dealer before you finalize the purchase. It outlines expected costs based on your initial negotiations, though adjustments can be made as terms are finalized.

Lenders rely on this invoice to evaluate your loan’s financial scope and confirm exactly what they’re financing. Typically, the invoice includes:

- Seller and buyer information

- A detailed description of the vehicle

- Estimated price

- Payment terms

- Validity period

For example, it should clearly break down costs like taxes and fees to avoid surprises later. Make sure the invoice is still valid when submitting it, as these documents often have expiration dates. To avoid confusion, ask the dealer to itemize all charges for better clarity.

Completed Financing Application Form

Once you’ve reviewed the vehicle’s cost estimates, the next step is to fill out a financing application form. This document officially kicks off the loan process and includes essential vehicle details as well as proof that you meet Uganda’s standard 40% down payment requirement.

Many dealerships offer tools to help you prequalify before submitting an application. For instance, if you’re considering a 2017 Subaru Forester priced at USh 60,000,000, you might expect monthly payments of around USh 3,195,398, assuming the standard down payment is made.

National ID or Financial Card

To apply for financing, you’ll need a valid government-issued ID. In Uganda, this is typically a National ID or a financial card. These documents not only verify your identity but also allow lenders to access your credit history through registered credit reference bureaus.

Make sure your ID is up-to-date. If you don’t have a driver’s license, other photo identification, like a passport, can work as well. These documents are also used to confirm your citizenship, which is often a requirement for local financing programs.

"It’s the law – a lender must verify your identity so they know who’s getting the loan." – Progressive

Documents for Individual Applicants

When applying, individual applicants need to provide additional documents to prove they can handle repayments and maintain financial stability. The exact paperwork depends on how you earn your income. Here’s a breakdown of what you might need to submit.

Bank Statements (6–12 Months)

You’ll need to provide 6–12 months of bank statements to show financial stability and that you’ve got reserves for emergencies. These statements reassure lenders that you can handle unexpected situations without missing payments.

If you’re making a down payment, the funds should have been in your account for several months. For freelancers and gig workers, bank statements often serve as the main proof of income and residence. Just make sure the deposits in your account match the income reported on your tax returns – any discrepancies could slow down the approval process.

Proof of Income

Proof of income is essential, and the type of documentation you need depends on your employment situation.

- For employed applicants: Submit your pay stubs from the last 30 days and W-2 forms. These documents confirm both your current earnings and your annual income history, giving lenders confidence in your steady income.

- For self-employed applicants: You’ll need to provide your most recent two years of federal tax returns and 1099 forms. Lenders may also ask you to sign IRS Form 4506-T, which allows them to retrieve your official tax transcripts directly from the IRS to verify your information.

If you have secondary income sources – like Social Security, rental income, investments, or spousal support – include documentation for those as well. This could be 1099 forms or bank statements showing the deposits. Highlighting these additional income streams can improve your debt-to-income ratio and strengthen your overall application.

Documents for Company Applicants

If you’re a business applicant, you’ll need to provide specific documents to prove your company’s legitimacy, financial health, and ability to repay loans. Here’s a breakdown of the key paperwork you’ll need to have ready.

Certificate of Incorporation and Company PIN Certificate

These two documents are essential to confirm your business is legally registered and operational. The Certificate of Incorporation establishes your company as a recognized legal entity, while the Company PIN Certificate verifies your registration with tax authorities. Lenders rely on these to ensure they’re dealing with a legitimate and registered business.

Audited Financial Statements (Last 3 Years)

Providing audited financial statements for the past three years is a standard requirement. These are crucial for lenders to assess your company’s financial health. They offer more than just a snapshot of your current earnings – they tell the "full story" of your financial journey over time. Lenders review these statements to confirm that your company has consistent income, sufficient reserves to manage emergencies, and a stable financial track record. Be prepared to explain any major fluctuations in revenue or expenses, as lenders prioritize steady income patterns when making their decisions.

Business Profile

A well-prepared business profile can significantly impact your credit risk evaluation. This document should outline your company’s financial strength, operational history, and creditworthiness. If the information aligns with data from credit bureaus, it can position your business as a top-tier borrower. This is a big deal because top-quality borrowers often secure financing with interest rates as low as 10%, compared to the usual 20–30% range. To avoid delays, double-check that the details in your profile match the records held by credit bureaus.

Additional Documents for Used Vehicles

When financing a pre-owned vehicle, lenders often require extra documentation in addition to the standard paperwork. These documents are crucial for verifying the vehicle’s value, confirming legal ownership, and ensuring compliance with import regulations. Here’s a breakdown of the key documents needed for used vehicle financing.

Original Market Valuation

A professional market valuation is a must for financing a used vehicle. This report helps lenders determine the vehicle’s current market value, ensuring the loan amount matches its true worth. It’s a safeguard for the lender, who typically holds an ownership interest in the vehicle until the loan is fully repaid. In Uganda, certified appraisers conduct these valuations, and their reports must include essential details like the make, model, year, VIN (Vehicle Identification Number), and current mileage. Double-check that these details align with your purchase agreement to avoid unnecessary delays.

Vehicle Logbook Copy

The vehicle logbook is a crucial document for verifying ownership and registration details. Lenders require a copy to confirm that you have the legal authority to use the vehicle as collateral for the loan. Starting in March 2026, Uganda’s government is rolling out a unified system that integrates the Tax Identification Number (TIN), Business Registration Number (BRN), and National Identification Number (NIN) to combat fraud. This system will make it easier for lenders to authenticate logbooks and cross-check ownership records, reducing the risk of fraudulent transactions.

Import Documents (If Applicable)

If the vehicle is imported, you’ll need to provide documentation proving it entered the country legally and that all taxes have been paid. These documents typically include:

- Bill of Lading from the shipping line

- Certificate of Conformity (PVoC) from approved inspection firms

- URA Customs Documents: Release Order, Exit Note, and Import Clearance Certificate

- Inspection Certificate from the Uganda National Bureau of Standards (UNBS), confirming the vehicle meets local standards

The estimated cost for clearance is UGX 12,804,428.04 (approximately USD 3,470), and processing can take anywhere from 1.5 to 7 days. These documents are essential for lenders to ensure the vehicle has no outstanding tax liabilities or legal issues, both of which could pose a risk to their investment.

How to Prepare and Submit Your Documents

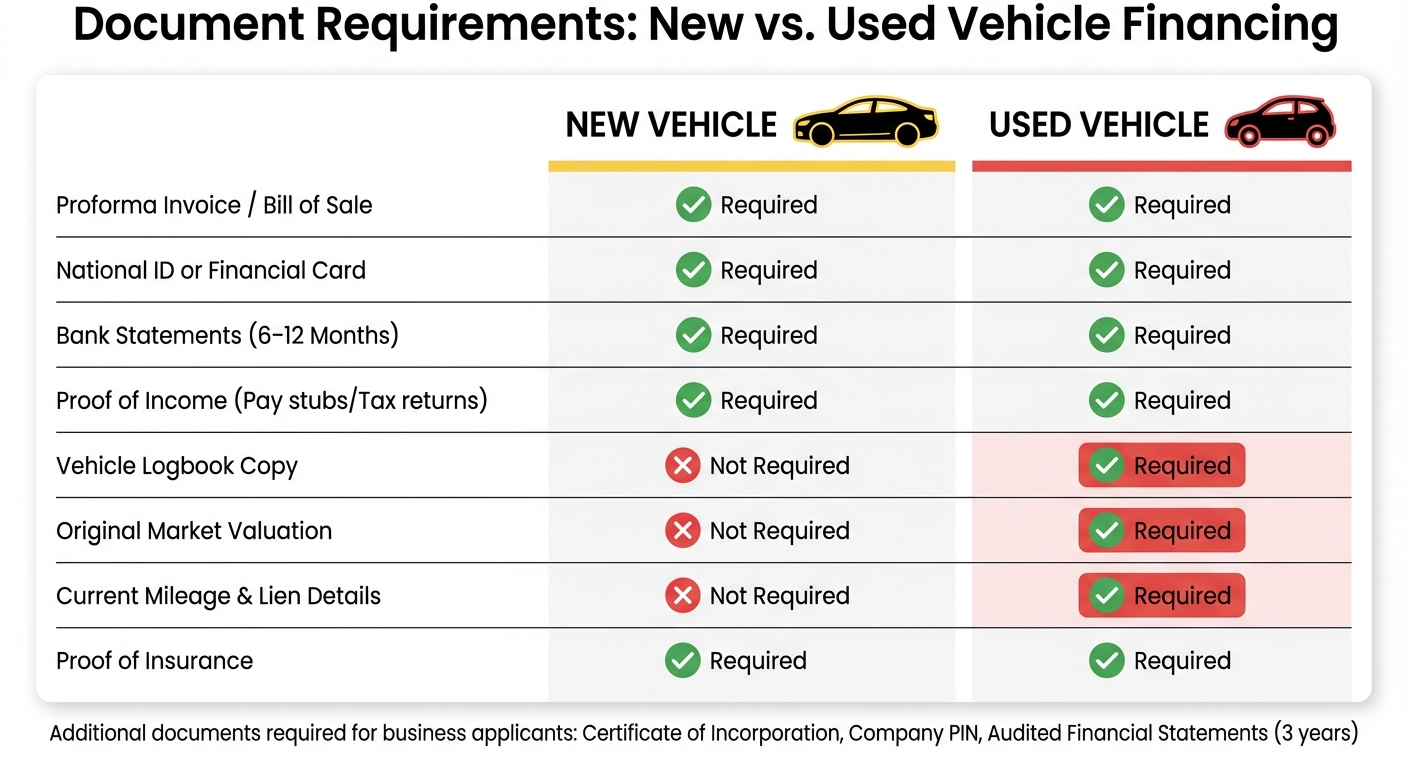

Document Requirements for New vs Used Car Financing in Uganda

Before heading to the dealership, make sure you’ve gathered all the necessary paperwork. This includes a valid ID, 6–12 months of bank statements, recent proof of income, and, if you’re self-employed, your last two years of tax returns.

For the vehicle, double-check that the VIN (Vehicle Identification Number) on the proforma invoice matches the car you plan to buy. If you’re trading in a vehicle, bring the current registration, title (logbook), and the payoff amount if there’s still an active loan.

It’s also a good idea to contact your insurance provider early. You’ll need to secure a binder or proof of insurance for the vehicle you’re financing, as lenders require this before you can drive the car off the lot.

Lastly, prepare your down payment in the correct format – this is usually a certified or cashier’s check – to avoid any delays in processing.

By following these steps, you’ll ensure your submission meets the dealership’s financing requirements.

Document Requirements: New vs. Used Vehicles

There are some differences in the documents needed for financing new versus used vehicles. The table below outlines these distinctions:

| Document Type | New Vehicle | Used Vehicle |

|---|---|---|

| Proforma Invoice / Bill of Sale | Required | Required |

| National ID or Financial Card | Required | Required |

| Bank Statements (6–12 Months) | Required | Required |

| Proof of Income (Pay stubs/Tax returns) | Required | Required |

| Vehicle Logbook Copy | Not Required | Required |

| Original Market Valuation | Not Required | Required |

| Current Mileage & Lien Details | Not Required | Required |

| Proof of Insurance | Required | Required |

For new vehicles, much of the vehicle-specific information is handled by the dealer in coordination with the lender. However, for used vehicles, you’ll need to provide extra details, such as the original title (logbook), current mileage, and any information about outstanding liens or loans.

Checklist for Complete Documentation

Before submitting your documents, take a moment to review this checklist to avoid any unnecessary delays:

- Bank Statements: Ensure they cover the full consecutive period required by the lender. For instance, if 12 months are needed, there shouldn’t be any gaps in the timeline. Even a single missing month could result in additional document requests.

- Proforma Invoice or Bill of Sale: Double-check that all details are accurate. This includes the VIN, make, model, year, and final purchase price. Any errors here could hold up your financing approval.

- Trade-In Vehicle Details: If you’re trading in a car with an active loan, confirm the payoff amount with your current lender. This helps the dealership calculate your equity or remaining balance correctly.

Carefully reviewing and completing your documentation ensures a smoother and faster approval process.

Conclusion

Getting your documents in order can make the financing process much quicker and easier. Be sure to have a valid government-issued ID, 6–12 months of bank statements, recent proof of income, and proof of residence. If you’re financing a used car, you’ll also need the original logbook, the vehicle’s current mileage, and details about any outstanding liens. This preparation ensures your dealership visit goes as smoothly as possible.

Being organized before heading to the dealership helps avoid unnecessary delays and keeps the approval process on track.

Don’t forget to finalize your insurance and payment arrangements beforehand. Make sure your insurance binder is confirmed and prepare your down payment as a certified or cashier’s check. Dealerships typically require both confirmed insurance and payment before releasing the vehicle.

For the latest financing options and detailed checklists specific to Uganda’s automotive industry, check out AutoMag.ug.

FAQs

What if I don’t have 12 months of bank statements?

If you don’t have 12 months of bank statements, don’t worry – you might be able to use other documents to prove your income. Many lenders or dealerships are open to alternatives like recent pay stubs or similar financial records. It’s a good idea to reach out to your dealership directly to confirm what specific documents they’ll need.

Can I get financed if I’m self-employed or paid in cash?

Yes, financing is available if you’re self-employed, but you’ll need to prove you can repay the loan. For those paid in cash, lenders usually require documents like bank statements or other records to demonstrate steady income before approving the loan.

What documents prove an imported used car is cleared in Uganda?

To ensure an imported used car is cleared in Uganda, you’ll need the following documents:

- Original passport with an entry stamp (or a copy if you’re a diplomat).

- Packing list written in English.

- Detailed valued inventory in English.

These are crucial for verifying customs clearance.

Related Blog Posts

- How Dealership Financing Works in Uganda

- Ultimate Guide to Car Financing in Uganda

- Avoid fake car deals in Uganda

- How to Finance a Car in Uganda: What You Should Know

{kind=link}